Last year was the year a lot of us were first introduced to stock market investing. It was an awesome and advantageous year for those who invested as much as a little of their money.

It was a bull market where the price of almost everything is increasing. We were all smart and made good money. On Twitter, I see a lot posting some 100% gain on some individual stock. In my opinion, there’s no better time to be introduced to the market.

Amid this endless opportunity to make money from investing, I had people messaging me about how they bought a stock and lost 30% or more of their capital. I felt bad for them and wished they didn’t lose the money but they did already.

So a bull market, a lot of people making money and some even losing money. Why should you then give up buying stocks yourself and subscribe to a Risevest plan?

PS: I am an independent writer and I’ve not been paid to write this.

The extra work may not worth it

Risevest’s ROI in 2020 was 41%. Yes, a whopping 41%. The implication of that is, without doing any extra work, without investing any extra hour to research, without spending the time for rest on your broker’s app, you could have conveniently made 41% ROI in 2020.

But is the extra work that you did worth it? Two things will help you answer that question correctly.

One, what ROI did you make on your portfolio last year? I’m not talking about ROI on an individual stock but on every stock that you bought (and probably sold) during the year. If that ROI is not up to 40% you may need to reconsider if you are good with what you are doing now or you would like to do something new. Let Risevest which is freely available to you be a benchmark. Also, while considering that, remember not to take for skill what is pure luck.

Two, if your goal of investing is beyond the return you make, then you may be fine. Even if you do not make up to the Risevest’s benchmark. I know this because 2017 when I started investing, my goal was beyond the money made. It included the education that comes with it, the emotion, the intellect, the mistakes and the wins. All added to me and have made me better today.

Otherwise, if all you are interested in is to focus on your work, and not have to disturb yourself about which stock to buy and which to sell, then going with a product like Risevest will be a great option.

Risvest ROI in context

It is not enough to use one year to judge Risevest as well and past performance is no way a guarantee of future performance. However, because they are an asset management company with a defined investment they may have a hedge over you. Also, unlike you, that is their day to day work. It is not justled with something else.

Yes, I cannot give them the pass mark just on one year’s performance. However, I am giving them merit based on the fact that they have a defined process, and it is their primary responsibility to make your money work for you. In order words, I can trust them enough to work to the best of their ability to make my money work for me while I focus on my primary which I enjoy or that is taking a lot from me already.

If you like ease and you don’t want to bother with which stock is trending or which is not, you may choose them and watch your money grow with them.

Fear, Greed, Hope and Ignorance are the 4 Apocalypse. Of the 4, the first 3 have to do with human emotions and they have together wiped out more wealth in the world of investing than any bear market had done in history.

The last one, ignorance has to do with the intellect. Ordinarily, it should be the only thing that causes us to lose wealth. Unfortunately, it is not even as harmful as emotion agents.

At the peak of GameStop’s fiasco last week, some people invested their life savings, some invested other people’s money, others their rent and the story goes on. As it would turn out, a lot of them were buying at the peak of the price. And now they have to painfully pay for it. Emotions ruled, greed prompted them to think they could make easy money and cash out, fear of missing out from the trendy was their guiding light and the hope that the price would rise again won’t free them from cutting their losses.

We are all subjected to these emotions, GameStop only came in as an example because of its recency. How many people bought Tesla for the same reason or Zoom or any other stock. How many have sold a stock because they couldn’t control their emotion or buy because emotion prompted them to?

Handling the apocalypse

Fear

Fear can drive us to either buy an asset or sell one. Fear of missing out will drive us to buy what you were not prepared to buy and fear of being in will force you to sell an asset you are supposed to hold. On both ends, knowledge and having an investment process will save you a lot. Knowledge about the asset in question and having a process about what to do when what happens is a saving grace.

I know emotion though, and I know we cannot always act according to reasoning from knowledge and process. So It may be wise to follow the process advised here.

Hope

Just like fear, hope works both sides of the market. You can hope that the price will fall further allowing you to buy at the bottom. Or you can hope that the price will rebound therefore holding your position instead of cutting your loss. Again, knowledge and process is your best solution here. Knowing what factors drive the value and paying attention to the behaviour of that factor is how you arm yourself with sufficient knowledge.

Here again, emotion will want to overpower you. My suggestion is that you note when you are being led by hope or by knowledge.

Greed

This is the father of all wealth destroyers. I will use an example of a trader here. If you are a trader, the most important skill you need to cultivate is to know when to take profit and move on. Ordinarily, you might have set that from the moment you enter your trade. But you see as your strike price approaches, the potential of getting more gains from the trade will entice you and you will adjust your analysis to accommodate your greed. That’s the beginning of failure. You see, we all want to make the maximum money from the market and this has cost a lot of us. Your goal as I’ve always said is not to make the maximum return in the market. Rather it is to make enough within your acceptable threshold or risk.

You will have to deal with your greed (and we all have it) to be able to control this horseman apocalypse who can turn your fortune into an overnight misery.

Ignorance

Ignorance should have been the cause of a lot of woes in the market unfortunately it’s not. However, it has its fair share of woes as well. A friend called me towards the middle of last year to lament how he has lost about 50% of what he invested in the stock market. How do you lose that much in a bull market? He’d bought stocks in an industry that was negatively affected by the pandemic. He was unaware. That’s the reason.

Ignorance can only be solved with knowledge. Get knowledge about whatever you are investing in and you will solve this easily. Remember the mantra, ‘never invest in anything you do not understand’. Well, that’s me saying it again.

2 years ago, I wrote here that the stock market can be as simple as buying and selling. However, what is most important is your motivation for buying and selling. Is it greed or fear or hope or ignorance for you? Be aware. The most optimal reason for your buy and sell of course would be knowledge.

Get knowledge, have a process, yield less to emotions and you will see your wealth grow with time. Fear, greed & hope have wiped out more money than any bear market in history.

WILKES-BARRE, UNITED STATES - 2020/11/27: A man wearing a face masks leaves Game Stop with the new Play Station 5 gaming console on Black Friday. (Photo by Aimee Dilger/SOPA Images/LightRocket via Getty Images)

When an unknown stock out of nowhere makes all the major headlines and takes over FinTwit, you will do well to pay attention to the story of what may be going on.

GameStop qualified for that description this week. Ordinarily, I don’t do so much as follow individual companies except they are interesting to me. So when GameStop started appearing here and there on my timeline, my default mode was to switch off my attention signal to it. But it persisted and I could not help but catch-up on the story. It’s a wild one and the most important lesson for me is that we can’t predict the future and the best we can do is to keep an optimistic view of it because humans will always find a way to progress.

So what’s the story?

A group of people on Reddit under the subreddit r/WallStreetBets (2.6 million members) saw that a stock has been shorted way too much. In fact, it would conveniently make the list of one of the most shorted stocks in history. Seeing that, they decided to organize one of the most popular if not the most popular games in the market. They started buying the stock. The result of buying the stock is that demand on the stock starts to rise. And as we learned from basic economics, when demand for a particular product/service starts to rise beyond the available supply, the price would naturally go up. That’s basic economics.

Shorting stocks means borrowing a stock today and selling it with the expectation that the price will fall further in the future. If it happens that things go as planned and the price falls further, the investor who borrowed earlier will simply buy the stock back at a lower price and return the borrowed shares. On the other hand, if instead of the price going up, the price starts going down, the investor who had earlier borrowed the stock will have to buy back the stock at a higher price in order to limit their loss.

That is, you borrowed it at $10/share and now the price is rising instead of falling, let’s say it’s now at $15/share. The investor quickly buys the shares at 15 so he can return to limit their liability. This process of quickly buying back to forestall liability is called short squeezing. The problem with this process though is that the more the investors demand the stock, the higher the price of the stock would go. They end up in a trap and the liability can be unlimited.

So as Redditors started buying GameStop, this happened and the hedge fund investors started losing money on an unprecedented level.

That’s story

What are the lessons?

No doubt, the coordinated effort is now successful. Let’s talk about ramifications.

Like I mentioned earlier, the most important lesson for me is that the future is unpredictable. If you think you could have seen what’s happening to GameStop coming and you could have benefited from it, you are still far away from understanding the workings of the world. Sure, if you were a member of the community that masterminded this, you would have gotten information and maybe benefited. Alas, you are probably not. The benefit of hindsight can be misleading many times.

If the future is unpredictable, what can we all do then? Betting on a future of prosperity is the most reasonable thing to do. Yes, you just need to be guided on how you place your bet. The world rose from abject poverty to abundance that it is today based on human ingenuity, I am not ready to write off that ingenuity today. It is such ingenuity that caused the hedge funds to lose billions of dollars today, albeit a market manipulation scheme. It is easier to win if you bet on prosperity than betting on failure.

How to bet on prosperity is to identify a company at the edge of innovation and scientific breakthrough and put your stake with them or otherwise, bet on the sum total of all human effort represented by the total stock market index. If these hedge funds had not tried to predict the future and bet on woe, this wouldn’t have happened. The butterfly flapping its wing did not set a good condition in this case for some. We could argue it did for those who masterminded the scenario.

Some other lessons:

Don’t ever short a stock

The future is unknown and optimism is more rewarding. Neutral is better than shorting, even if you are convinced of an impending end. If you think you are very convinced that the stock will go one way, ask the hedge fund guys where their conviction brought them. If you think it cannot happen to you, you have not read enough articles on this blog, “risk always looks impossible until it happens” is an intrusive statement.

Believe rather in prosperity and invest accordingly.

Retail Investors have become more power

Throughout last year, comments were flying here and there about how Robinhood traders who don’t understand the market are pumping share price up. Some professional investors would probably have wished such access wasn’t made available. Unfortunately, it is available and can’t be taken away again. And the retail traders have demonstrated in the past 14 months that they have enormous power over the market just as much as the big guys could have. Always put that into consideration going forward.

This is not the end, legal possibilities

Market manipulations are illegal in the market, and this is a whole new dimension to it. So expect the men of the law to step in at a point in time. We will have some new guidance.

If you are conversant with this blog you would have learnt that I like simple things. I like my investment process to be as simple as possible, I like writing to be as simple as possible and I like to do things that will allow me to have a night sleep. The downside to my simple lifestyle is that I may not make the highest return in the market but I can be sure that my capital can stand the storm and that over a long enough time, I will outperform more than 80% those who complicate investment decisions.

Don’t get me wrong, doing simple things has ramifications. It could be buying a low-cost Index ETF over and over again, it could be buying a specialized ETF or it could be a combination of both mentioned already. And yes, it could also be doing the hard work to find the next Amazon or Apple and averaging in on them for the next 20 – 40 years of my working career. The idea is that keeping one’s investment process as simple as possible has dividends that surpass the alternative.

To further my agenda of helping you get wealthy through the practice of investing, I want to share with you 3 core principles that should guide all your investment decisions. These are principles that will serve as a light for you every time you want to put money into something and when you want to get it out.

Don’t lose

Whenever the issue of money comes up, our first instinct is always how do I make more of it. How do I double this amount of money in this short period? As Tony Robbins put it in his book, the best investors are obsessed with avoiding losses because they understand a simple but profound fact: the more money you lose, the harder it is to get back to where you started.

Let me put that statement in perspective for you. If you invest N100,000 and lose 50% of it, bringing your capital to N50,000, how much would you need to get back to N100,000? You may be tempted to say all you need is to make the 50% that you lose back. However, you would be wrong because turning N50,000 to N100,000 requires a 100% return. And 100% is an unprecedented number that may take up to 10 years depending on what you invested your money in.

This explains why Warren Buffett 2 rules of investing are, one, never lose your money and two, never forget rule number 1. The rules are instructive enough.

Never lose your money doesn’t however mean you should not invest your money at all or that you should avoid making more money in the name of not wanting to lose money. You would be wrong to think that way because even the Buffett himself is a legendary investor. So what does it mean to not lose money?

Don’t invest in what you do not understand. Doing so would ordinarily force you to make investment decisions that will cost you money.

Don’t risk too much of your capital.

Define your investment strategy and stick with it

Don’t chase the highest return in the market rather invest in what will give you a great sleep at night.

Aim for being reasonable over being rational. Humans are emotional and we can’t be rational all the time but we can be reasonable all the time. That’s why I wrote this article on how to deal with the fear of missing out.

That’s not all but I’m sure those would give general guidance about things you can do to lose your money. High returns are good, doubling your money is fun. However, not losing what you’ve worked hard to earn is even more rewarding and it’s a lofty aspiration and easily attainable goal.

Asymmetric risk/reward

While I was learning corporate finance, what I was taught was that the higher the risk the higher the expected returns. In order words, I should not expect higher returns except I’ve assumed a higher risk. And I think there is an element of truth in that no doubt. Yet, one of the best things you can do for your investment is to look for opportunities where the reward is really high relative to the risk you are taking. It’s called asymmetric risk/reward.

Let’s use numbers a bit. Imagine you have N1m to invest and you take 10% of that (N100k) to invest in an asset that returns 500%. That is to say, your N100k investment is now worth N600k. Even if you only made a moderate 10% on the remaining N900k, your new net worth at the end of such period would have become N1,590k N(900k + 90k + 600k). On average, your investment had made a return of 59% on your invested capital.

The temptation when one finds an asymmetric investment is to want to bet more than what is reasonable and prudent. Remembering the first guiding principle should be a guide here. Asymmetry investments are not definite, just as much as they can increase greatly, they can also reduce erratically. That’s why putting a moderate amount of money is always the optimal hedge. Thinking about our example from above, if you lose 50% of the N100k, overall, your portfolio will still stand strong because your total balance at the end of this scenario would now be N1,040k N(900k + 90k + 50k). In which case you would have been true to the first principle of not losing your money.

And asymmetry investments are always available even though it is only the benefit of hindsight that makes them obvious. To mention a few, Apple, Microsoft, Tesla, Bitcoin, Starbucks are a few that will qualify for an asymmetry bet. The relevant question as you will agree with me is which investments are the next asymmetry bet? Well, they are always known absolutely until it’s too late. Keep an eye out is my response to that.

Are asymmetry opportunities only available in the public market? The answer is no. Some get their asymmetry returns from private investments like investing in startups, some times, it could be just a friend introducing you to something from nowhere but which you feel confident enough to invest in. It can come from anywhere.

Diversification

The third one is obvious. We’ve all heard the statement “don’t put all your eggs in one basket”. But what does that mean? There’s a difference between blindly quoting a statement and knowing what it means plus doing it.

I learnt something interesting from Tony Robbins on the different kinds of diversification. I will share them with you because they are important.

There are 4 ways to diversify effectively:

Diversify between assets within different classes (e.g., real estate, stocks, bonds, commodities, private equity)

Diversify your holdings within asset classes (avoid concentrating putting all of your money into one stock or bond; you must diversify even within your asset classes)

Diversify globally (e.g., markets, countries, currencies) – if you live in my part of the world where the currency depreciates very often, this point is even more important for you. Having some of your investment in a dollar-denominated asset, some Bitcoin, if you believe in it, would be a practical way of going about this.

Diversify timelines (e.g., dollar-cost averaging, maturity date) – you are never going to know the right time to buy anything. But if you keep adding to your investment systematically over months and years (that is cost averaging), you’ll reduce your risk and increase your return over time.

All the principles mentioned so far are easy to repeat and read but doing them can be difficult. That’s the nature of simple things, they are difficult to implement but those who implement painstakingly are always rewarded. That’s why I like the wisdom of Charlie Munger when he said: “take a simple idea and take it seriously”. Doing so will put you in the top 10% of the world’s best I believe.

Are you a polymath? Someone that wants to do a lot of things, you see yourself creating a massive empire in a lot of unrelated areas. You just want to do a lot of things or you are even doing them already. However, you noticed the results aren’t forthcoming, or importantly, you realize that the world wants you to pick one thing from all.

I used to be like that or I still am. I want to be 10 different things at a time, I want to have a successful corporate career, I want to create a successful startup, I want to be an investor and on another day I want to be an inventor as well. It’s a lot of things for one person. And you know what, anytime I remember each of those my “want to be’s”, I launch into research on them again. In the end, all those efforts amounted to nothing. Stuck is a more generous word to use for my situation and “being a donkey” would be a perfect word to use.

Let’s get something straight immediately, in this one life that you and I have, we can’t be everything that we possibly want to be. Enough of the “you can whatever you want to be”. Really that’s BS at best.

That said, we can be as many things as are important to us. We just have to stop thinking short term. I do all those my “want to be’s” because I used to think I must be everything right now or never. That’s why I’ve never got anything done until I changed my approach.

Thinking long term is the goal solution

Thinking long term affords us to see life differently. We have all agreed that we can’t possibly be everything that we want to be. However, we can be more than one thing in our lifetime.

Thinking long term means you allow yourself to be one thing per time. Be one thing for a few years, whenever you think you’ve done enough of that thing, gained mastery and accomplished enough, then take the next thing to do. Of course, the idea is that you have the time to do all those, and even if you don’t, the world will benefit more from the result of your extreme focus on one thing than from the dispersed focus you have for a lot. That’s because things that endure and change generations are built on those kinds of foundation.

And like I noted in this article, “another success” is always easier after the first success. You would have proven yourself worthy, capable and deserving of the resources that are required for the next adventure once you can show a result from previous wins. Do you remember that parable of the talent? You saw how those who made initial success were rewarded with more resources to have more success? And don’t forget the one who was into a lot of but had no success, even the little he had was collected from him.

What’s the donkey’s story?

A Buridan’s donkey is standing halfway between a pile of hay and a bucket of water. It keeps looking left and right, trying to decide between hay and water. Unable to decide, it eventually dies of hunger and thirst.

The donkey couldn’t think long term. If he could, he’d clearly realize that he could first drink the water, then go eat the hay.

“Don’t be a donkey. You can do everything you want to do. You just need foresight and patience.

If you’re thirty now and have six different directions you want to pursue, then you can do each one for ten years, and have done all of them by the time you’re ninety. It seems ridiculous to plan to age ninety when you’re thirsty, right? But it’s probably coming, so you might as well take advantage of it” said Sivers. He continued “You can fully focus on one direction at a time, without feeling conflicted or distracted, because you know you’ll get to the others.”

And while you are at that, never forget that most people overestimate what they can do in one year, and underestimate what they can do in ten years. That statement is always true. I’ve chosen to be extremely focused on one thing per time now and I’ve seen an amazing kind of result. This year, this website is my project. Let’s see what one year of extreme focus will bring me.

True riches come from your income source not how you spend your income. And investing is a function of how you spend your income.

My first salary when I relocated to Lagos was 70k/month. With such an amount, no matter how much I save, before I could have a million naira saved up, it might take between 1 year (if I save everything that I made) to 11 years (if I save just 10% of that income). That’s assuming of course, that I did not get an increase in income.

Good enough for me, I got a new job that allowed me to save about a million naira within the first 1 year on the job. Can you see the point I’m getting at now?

Savings and investing is good. A habit that must be cultivated else, one will remain in perpetual poverty. However, obsessing over saving and investing the small amount one earns instead radically working to increase one’s income is an ill-informed obsession.

I tweeted recently that I would rather have a 5% ROI on an N100m than rejoice over 200% on N10k. The reason is obvious, the former gives me a larger capital and eventual N5m ROI, while the latter despite its high percentage only leaves me with a paltry amount of N30k.

Been preaching this since. What's the point of a 200% return on N10,000.

And that’s why they that look for high ROI are usually those with small capital base. When you have large capital even a 3% “guaranteed” ROI would do you much good. That’s usually so because one, you don’t want to lose that capital since you must have worked really hard to earn it and two, since it’s large enough, little percentage returns are usually big enough to take care of your moderate lifestyle.

The goal for everyone who’s looking to make wealth is to ensure that they do everything within their power to increase their capital base. And that only comes by increasing your earnings. Savings and investment is a practice along the journey to riches that ensures that you preserve what you earn and grow it. It’s not a substitute for increasing your earnings capacity and it will never be.

So when I say investing will never make you rich, I don’t mean it literally. But that obsession over-investing at the expense of increasing your income will keep you in the poverty that you aim to escape. Just imagine if I’d remain in my first employment with no salary increase and I had to take 11 solid years to save up to N1m. That’s cruel.

How to increase your income

I have seen people take all their savings and liquidate all their investments just to use it to pay for a professional exam. To the uninitiated, it looks foolish. They will wonder why will you not have an investment, why can’t you think long term and play to the tune of compounding, why are you so short-sighted? I will tell them to shut up. Yes.

You see, the biggest investment you can possibly make is an investment in yourself. An investment in yourself will return the highest ROI. And educating your mind is how you invest in yourself.

Let me ask you a few questions. Since you know that investment is the principal thing, why didn’t you save all your school fees and invest it in someplace instead of going to school? Why did you choose to go to school first? Isn’t it because of the school that you went to that is giving you some leverage to earn an income now? So why did you all of sudden think investing instead of more education (skill) would salvage your money problems?

You see, your income problems can’t be solved by investment in assets but an investment in yourself via the acquisition of more knowledge. That could be by taking professional exams or learning a new skill, or learning how to do something differently. Basically, it has to be an investment in yourself. That’s how you increase your income.

It is you that earns the income. When you are about to be paid, you will be paid based on what you have in your head and can do with your hand. Not what you have saved up and invested. Always remember that.

Join 400+ people who are subscribed to my newsletter via this link to get notified of future posts like this and more.

I was reviewing some data when I realized a lot of people are seriously wondering and interested in the answer to the question of if they should use Rise for their investment or Bamboo and its alternatives (Trove and Chaka).

First, it gives me joy that you are thinking about that. It means you want to do what’s best for you. You want to leverage on an advantage that no generation before us had. Secondly, I should mention to you that your goal is to save your money, make more money and not lose your sleep in between. It’s not to show off on anything at all.

Difference between Bamboo and Rise

– Bamboo

Bamboo is a trading platform that allows you to buy stocks and hold until you wish to sell.

Bamboo provides the platform where you can buy an individual stock, ETF, Inverse ETF or anything that is listed on US stocks exchanges. The responsibility of knowing what to buy and when to buy it rest on your shoulder. And so is the responsibility of knowing what to sell and when to sell.

Full control lies in your hand. Bamboo makes money from you by charging you a trading fee on every transaction. When you buy and sell you get charged for those activities.

Note: everything I have said and will say of Bamboo is the same for Trove and Chaka since they have the same business model.

– Risevest

Rise on the other hand is an investment manager that offers different investment products for you to choose from and invest in. The three products currently being offered are

Fixed Income – a form of investment whose return and maturity are fixed and determined from the inception of the investment. That is, once you invest, you can’t withdraw your money at any time until maturity and you are fairly certain about what the return will be upon such maturity. You may actually withdraw before maturity but you will have to pay some charges. This is considered low risk because it is a debt instrument with collateral

Real Estate – this works like fixed income as well. You have to hold it until maturity which you would set from the beginning, and you can’t withdraw your money anytime before that maturity hence you will pay some charges. The difference is that you can’t tell ahead of time what the return on investment would be. However, since it is a fund that invests in properties with rental income in the US, it’s a great product as well and consider medium risk.

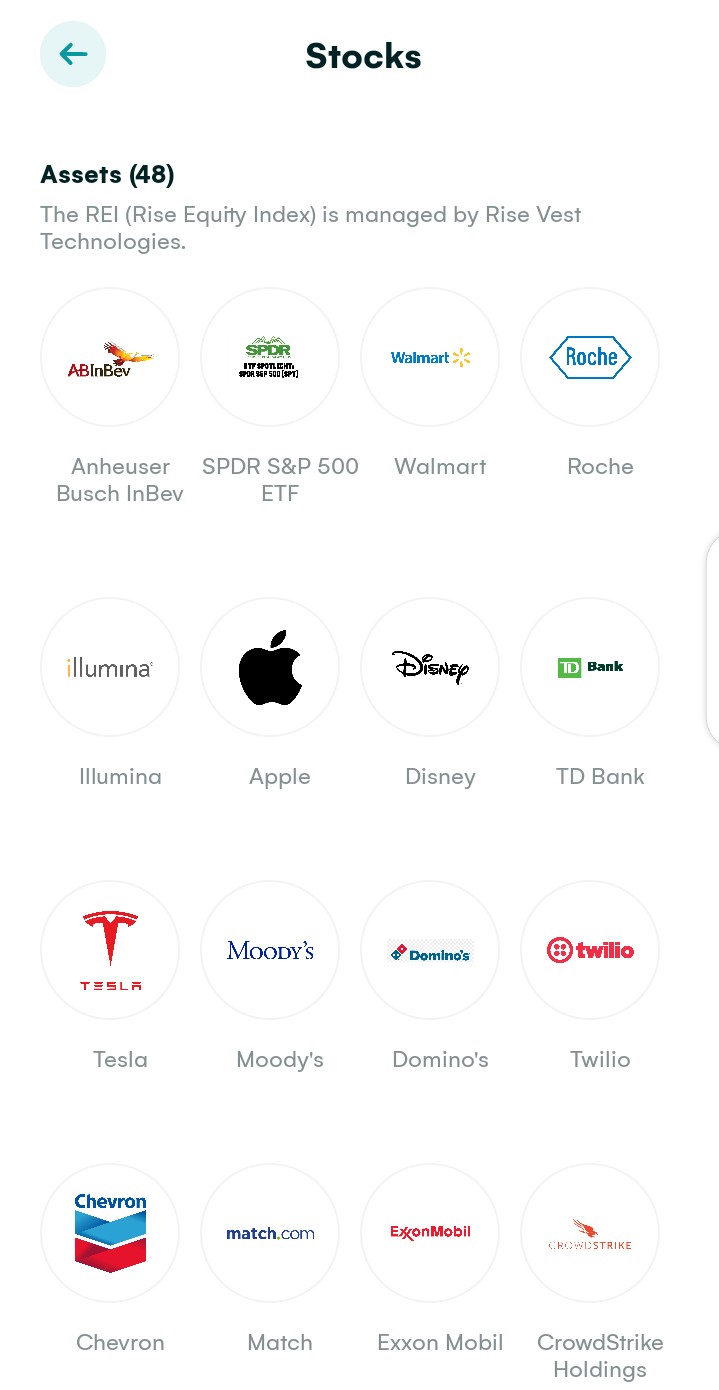

Stock – risevest selects some good companies listed in the US and just like an ETF would operate, they invest your money in that basket of good companies. If you invest $100 for example, you would be buying as many stocks as is in that basket at the time. And what’s in your basket changes as often as Risevest changes it.

It’s called Rise Equity Index and currently has 48 stocks in the basket. Rise has often said that their goal is not to beat the market but to select a couple of great companies to invest in and if that beats the market, it would be great. That is the right way of looking at things if you ask me. It’s an appropriate optimization. 2020 performance is yet to be made public but 2019 was 19% for the number of months they were in operation.

Rise currently makes money from what is called a management fee. They charge up to 2% on total assets under management on the condition that you make a minimum of 10%. Read more about that here.

Which one should you choose?

Now that you understand the difference between both, it’s only fair for you to consider which one you should choose. To start with, nothing is stopping you from using both of them if you so wish.

With that in mind, if you are the type that does not want to go through the rigour of having to search for what to buy in the stock market then Rise is the best option available for you. If you are not interested in all the euphoria that owning an individual stock brings, and you don’t want anything more complicated than you already have in your day to day life, then Rise would probably just be perfect for you.

Also, if you want to exposure to other assets like fixed income and real estate, only Rise offers that. If you don’t want to take on a lot of risks and can’t bear seeing your money occasionally give negative returns, then Rise products are your best option. It’s the simplicity that makes Rise stand out. All you have to do is deposit your money and with few clicks invest your money.

On the other hand, if you are interested in the workings of a business, you want to know how the stock market works, you are ready to pay the price of putting your money in the stock market then Bamboo and its alternatives (Trove and Chaka) is a good go. If your goal is to trade in the market, also Bamboo is the way.

By the way, trading means buying and selling of stocks within a short period of time. Investing on the hand is done with a long term view.

However, this is not a rule and nothing should stop you from using both services if you so wish. But your goal again is to save your money, make more money and not lose your sleep in between. Don’t optimize for any other thing. Don’t allow the fear of missing out to push you to do what will make you lose your money. It’s your hard-earned money and your number one responsibility to that money is not to lose it unnecessarily. That’s an important responsibility even before multiplying the money.

Join 300+ people who are subscribed to my newsletter via this link to get notified of future posts like this and more.

I, like many others, have used the word “dollar cost averaging” countless number of times. We use it when asset prices are going up and when they are going down. We treat it as the holy grail for the rational investor. But never has anyone put it in proper perspective as I am going to put it for you in this article.

The concept of (dollar) cost averaging means if you have a lump sum, $1,000 to invest, instead of investing it at once, you spread it over let’s say 10 months and buy $100 in each month. That’s usually advised because you are not sure if the asset (ETF or Stock) is at its peak by the time you want to buy it or not. As such you should avoid buying the asset with the lump sum and do a cost averaging instead. That way, you even out the effect of buying at the top and benefit from different swings that may occur during your buying period.

What that implies is that if all you do is to take $100 out of your salary every month to invest, then that’s not cost averaging. That’s just doing what is only feasible and available.

Although now, we call everything cost averaging. That’s fine. Let’s bother about the substance here and leave forms alone.

That said, what advantage can cost averaging have? Or even taking an amount daily/monthly to invest in an asset?

The perspective

One of the biggest dilemmas that we all face whenever we want to invest is what if the asset (ETF, Stock, Bitcoin etc) is currently trading at its peak price. Meaning once you buy it the asset probably stops growing or starts to decline. That’s not something that anyone wants even if they are keeping a long term view as expected.

(Dollar) cost averaging is the buying strategy that will come to the rescue here.

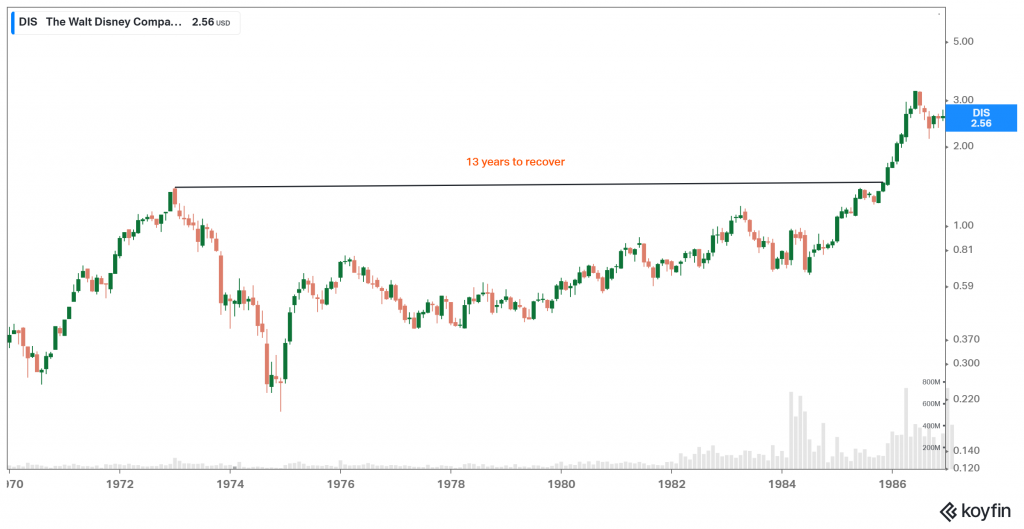

Example 1 – Let’s assume the date is September 2018 and you have just been introduced to stock market investing. Having gathered enough understanding, you chose to invest in Amazon stock, being a good company with strong fundamentals. Unbeknownst to you, Amazon was trading at its peak price that day as shown in the image below. And for the next 200 days, the price didn’t recover back to that peak price.

If you employ the strategy of cost averaging, during this period, you could still have made a return of about 17% on your investment.

The assumption for this particular calculation is as follows.

Your first purchase was made at the highest price and you bought one unit of Amazon shares.

You bought one share every trading day of the week for 200 days until recovery. By implication, at the end of that 200 days, you own 200 shares of Amazon.

At the end of the period, you would have invested a total sum of $345k and the value of that investment would be $403k. Giving you about 17% ROI even though technically, there’s been no growth for the asset over that 200 days.

Example 2 – the same argument and process are involved here. Your first purchase was at an all-time high after which the price started to decline. Except that here what we are buying is an ETF. Despite no growth in asset value over the 150 days, you still made an ROI of 9%.

The explanation here is that buying on a scheduled interval pays off over the long term. I’ve assumed the worst scenario to say you bought at the peak then the price starts to decline. Yet, you can see how you can still make money in such a chaotic situation.

The alternative to that of course is to try and time the market. But if you have tried that before, you will agree with me that it is a skill that ranges from difficult to impossible to achieve. That’s accompanied by a lot of headaches.

That’s why this favourite article of mine is so relatable – Just Keep Buying

There’s a problem with that strategy though. It assumes that the asset price will recover and they don’t always do.

The only criteria for cost averaging to make sense

Now that you understand the perspective with a real-life scenario, I want to tell you the only criteria where the strategy makes sense.

As you’ve seen, I used an extreme example. A situation where your first purchase was at a peak and it continues to decline and didn’t fully recover until some 200 days later.

The only question you have to ask yourself then is, will this assert ever fully recover and return to growing? Once you are optimistic that it would, then you can proceed with your investment till forever.

That’s a big question though and it can be really difficult knowing which asset will recover. It’s the reason why I have a bias for board market ETFs. Because betting on them would be betting on the entire human ingenuity. And if history has taught us anything, it’s that human ingenuity will always prevail.

And in case you don’t know, not all individual stocks recover and while some may even do, they may take longer than what the human capacity can bear.

All assets don’t recover from a fall

Let me share a couple of examples of assets that never recovered or took way too long to recover.

Microsoft took 14 years

Walt Disney took 13 years

I could go on but you get the point already.

On the other hand, if you bet on a broad market ETF for example, you can almost always be sure that they will recover and it won’t take long.

These are the huge falls and recovery of VGT during 2020, 2018, and 2008. All recovered and as noted above, you would have made a 9% return during the 2018 fall.

Same goes for SPY and VTI check them out. Learn from history.

Now you understand cost averaging what’s stopping you from leveraging it. Will you allow greed, fear, hope and or ignorance the 4 horsemen apocalypse of the stock market to hold you back?

Join 300+ people who are subscribed to my newsletter via this link to get notified of future posts like this and more.

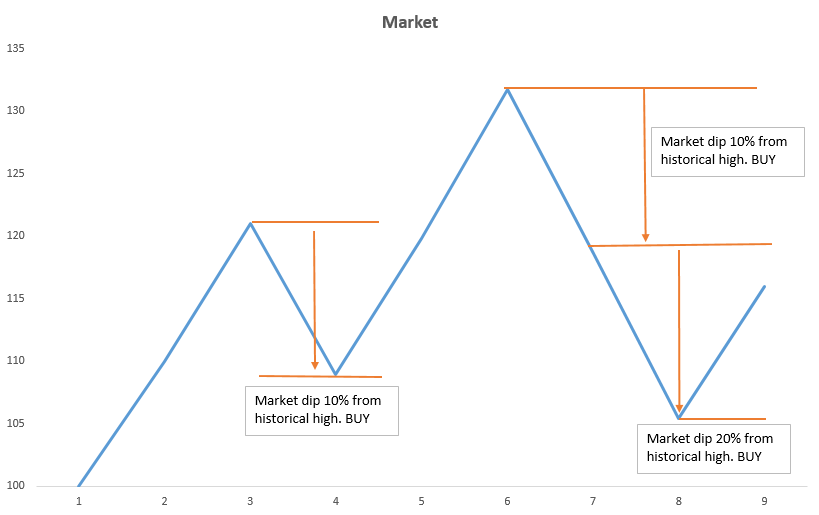

Did you buy the dip? he asked. After waiting for 24 hours and an eventual rally, not a single soul came out to say they bought the dip (price drop). That is how the story always starts and ends.

Whenever an asset price rises, the quest to benefit from such a rally forces everyone to want to get on the train. Unfortunately, the rally gets so high that everyone is now waiting for a drop in price before they buy the asset to benefit from its rally back to the top again.

The fortunate thing is that every asset almost always has this dip that everyone is waiting for. Unfortunately, almost no one would have the mental fortitude at that time to buy what they’ve been waiting for. This phenomenon surprises me. So I pondered on it to come up with an explanation of why that is and a possible solution or way forward.

This is why no one ever buys the dip

Psychology – we are not wired to process such a scenario properly as humans. We like our money and accepting loss is not our forte. Buying a dip means the value of your asset may start declining immediately after your purchase. What we are psychologically wired for is to assume the dip is not dipped enough yet, hence we should wait till it’s deep enough before we buy. Unfortunately, knowing when we have reached the bottom of the dip is close to impossible and so we all miss buying the dip. Ordinarily, an asset price would then stabilize at the dip or start to rise again. The problem is we can’t time any of these events. And our inability to time it is the primary reason why we don’t usually buy the dip.

Volatility – we don’t know if it will rally again or not and if it does, we don’t know when. When a dip starts whether you buy the dip or not depends on your estimation of how deep the dip can go and how soon it will recover. For a very volatile asset like Bitcoin, it’s almost impossible to tell all those variables and that makes it even harder to buy the dip. The more volatile an asset is, the harder it is to buy the asset’s dip. For context, there’s nothing and I mean nothing stopping Bitcoin from losing 50% of its value in a very short time and there’s no promise as to when it will recover that back. This makes it difficult to buy any dip. How deep a dip can go relative to the time it would take for the dip to recover is a metric that would determine how easy it is to buy a dip.

It is possible to buy the dip

Buying the dip is easier and often possible if you have a long term investment horizon and you are investing an amount of money that would not materially affect your lifestyle if you do not have access to the money for a very long time.

I bought (all) the Bitcoin dips for example. Yes, I meant that. I bought all the dips but I also bought all the highs.

“Time in the market is more important than timing the market”

Every now and then, I transfer a given amount to my Luno wallet and automate a daily purchase of some Bitcoin. By implication, whether Bitcoin is high or down, dip or all-time high, my order will be executed. However, since I am not making a one-off purchase, the impact of any one purchase on any given day will not materially affect my returns.

If I bought at an all-time high, it would just be a one day purchase out of many other days that I’ve been buying and that won’t have any significant impact on my overall returns. The same goes for buying when there’s a dip. As long as my standing order is there, it doesn’t matter if it’s a dip or all-time high, the order gets executed.

Buying the dip has only been made possible for me because of that practice. If I’d had to buy it myself, I can assure you just as you couldn’t, I wouldn’t have bought it as well. I am no special human and I have the same genetics of fear and greed as anyone else. It is how we manage it that differentiates us.

Also, I could successfully do that because I am holding a long term horizon for Bitcoin. The last I checked my account, for instance, I’ve made >130% from my boring daily standing order. But I had no urge to sell and I don’t mind if I lose all that huge percentage returns. I will only have more opportunity to buy the dip.

If you think you can do otherwise, i.e. buy the dip yourself, you overestimate yourself and know little about yourself. You can’t buy the dip except you have those two things well thought; your time in the market (how long you want to be invested) and the kind of money that you have in the market (if it won’t affect their livelihood).

But seriously, did you buy the dip? I’m curious.

Join 400+ people who are subscribed to my newsletter via this link to get notified of future posts like this and more.

The question I get at almost every passing week on Twitter is “David, I’m new to this stock investing thing, could you please tell me where to start and what stock to buy”? I have tried to answer as many people as I can, but I believe it’s time I answer this question more extensively for everyone.

The world did not start knowing prosperity until the 1800s that marked the beginning of the industrial revolution. It was the age when we moved away from scientific invention to innovation. From then on till today, the growth never slowed down again. We basically accelerated.

The industrial revolution ended and the information age even did more to growth in the shortest period of time. Much faster than the rate at which the industrial revolution did. The industrial revolution used 150 years to move the average global GDP per capita from $2,000 to $10,000. While the information age that started in the 1950s has moved that $10,000 to about $40,000 for the most advanced countries where these were all pioneered.

The United States of America was the epicentre of this growth. The United States under titans like John Rockefeller, Andrew Carnegie and Elon Musk, Jeff Bezos, for our generation pioneered the finest businesses of this era. They built companies that grew in value and the American population participated in prosperity share via investment in the stock market. They made a fortune from this market just as the builders made. There is a popular story of Grace Grooner recounted by Morgan Housel. She died a millionaire despite being a secretary throughout her professional life.

It is absolutely understandable for us outside of the United States to desire to benefit from this opportunity.

However, up until now, this prosperity has only been enjoyed by Americans alone who invested their savings in the stock market and watched its value grow tremendously and even predictably. While other countries also have their stock market, not one of them has delivered the kind of prosperity that the US stock market has delivered since it was founded in 1792. Hence, we’ve been left out.

I am fond of saying my generation has an unequal advantage to build wealth that any generation before us did not have. I still stand by those words and this sentiment applies to all countries where once the ability to invest in the US stock market wasn’t available but now is.

With this knowledge, how can you invest to benefit from the massive opportunity?

Our basic instinct to the stock market

The basic instinct of anyone when first introduced to the stock market is to see it as a place where they can put a buck and quickly make some gains. After which I like to ask them what next? What if the company’s stock is still going up? Would you buy again to make another buck or will stay away from the company entirely.

Usually, I see that as an unnecessary mental dilemma.

Let me go straight to the point to say that you may stop reading this post of what you hope for is some strategy on how to do something like that. To buy and sell and find the next to buy which is basically trading. This article isn’t for you. It is rather for those who plan to utilize this opportunity to build long term wealth.

The first question every individual who is getting involved in the stock market has to answer is the question of why they are there. Why have you come to the stock market, to invest or to trade? No one is more honourable than the other by the way. However, if you do not decide ahead of time why you have come to the stock market, you’d be playing the fools game.

I like the words of Benjamin Graham on this point.

“There is intelligent speculation as there is intelligent investing. But there are many ways in which speculation may be unintelligent. Of these, the foremost are:

Speculating when you think you are investing.

Speculating seriously instead of as a pastime, when you lack proper knowledge and skill for it; and

Risking more money in speculation than you can afford to lose.”

So it is important to determine in advance Which table you are on. Else, you would be doing unintelligent investing in general.

I assume you are here to learn about investing and not speculation.

Two investment parts

There are two broad ways to participate in the stock market. Once you invest in a basket of stocks already selected using metric. And two, you pick the individual stock yourself.

Again, none is more honourable than the other once you know what you are doing.

However, over time, we have learned that the idea of picking stocks is not something everyone can do. The sheer amount of what it requires to know how to, plus the probability of any individual consistently outperforming the broad basket of stocks approach has proven that at best no one should go this route except they are willing to do the work that needs to be done.

I must mention at this point that this has nothing to do with your level of intelligence as much as it has to to do with how the market itself works. In 2007, Warren Buffet placed a bet together with a hedge fund manager (one of the most sophisticated types of investors) that over a period of 10 years, they wouldn’t outperform the S&P 500 net of fees. By the time the bet matured in 2019, it was so that they didn’t outperform the “basket of stocks”. So even the most knowledgeable could underperform what they were usually employed to outperform. So it’s not just about you when I say you may not outperform the “basket of stocks” option.

It is in light of this that my usual investment advice for anyone including me is to go for the “basket of stocks” option.

The basket of stocks is called an ETF for our sake. An ETF can either be passive or active.

Passive ETF

Passive ETFs track an index. For example, SPY is an ETF that tracks the S&P 500. S&P 500 represents the top 500 companies listed in the US. There is a standard requirement for companies to be added and removed from the index. That’s something you don’t need to bother about. Passive means no one is buying and selling stocks in the ETF every other day. The only time things change in the basket is when the condition to add or remove a company’s stock from the index is triggered. I’m glad we witnessed that lately with the addition of Tesla.

The characteristics of ETFs like this is that they are always low cost. That is, their expense ratio, which is the cost of managing the basket is always lower compared to the actively managed. They range from 0.01% to 0.1%.

Join 300+ people who are subscribed to my newsletter via this link to get notified of future posts like this and more.

Active ETFs

Active ETFs on the other hand is being actively managed as the name implies. Okay, that’s like a tautology. What it simply means is that there’s usually a manager behind the wheel who on a daily basis decides whether to add stock in the basket or remove from it.

ARKK is an example of such an ETF. Usually, they always have a theme and the theme determines what kind of stock is added in the basket. The theme of ARKK is innovation, so stocks that are highly risky but innovative are what gets added in the basket. There might be another that tracks Cryptocurrency assets or Oil assets or Fintechs and so on.

As you would’ve guessed, the implication of active management is a higher expense ratio. It usually ranges from 0.3% – 2% if not more. ARRK here, for instance, has an expense ratio of 0.75%.

The most important thing about investing in an ETF is that it takes away from you the burden or task of having to research an individual stock. Which would also require that you often have to check if your assumption for buying them still holds especially in times of massive sell-offs. Of course, the cost of that is the expense ratio you will be charged which is fair.

You will notice that so far, all I’ve been doing is put you in the right frame of mind and arm you with the necessary knowledge. That’s the way it should be. Knowledge of the market you want to start getting involved in is critical. I won’t also be talking about stock picking as I don’t encourage it. And not even when you are new. Also, because what the majority of us can do and do successfully is this type of investment. Stock picking is another game.

What’s the next step?

ETFs You Can Buy and Sleep

What would constitute for you an acceptable average return per year? Often, it is said that 10% ROI on your investment per year for 10 or more years is a good deal. In fact, some may say that’s as good as it can ever get. I don’t contend with that and I would also rather have that than have anything less.

These ETFs have historically given that minimum returns or even more. Take a look at them and decide for yourself which one you want to invest in. Ordinarily, one or two is usually enough. Once you have decided, all you have to do going forward is to buy some amount monthly that you can afford to invest for the long term.

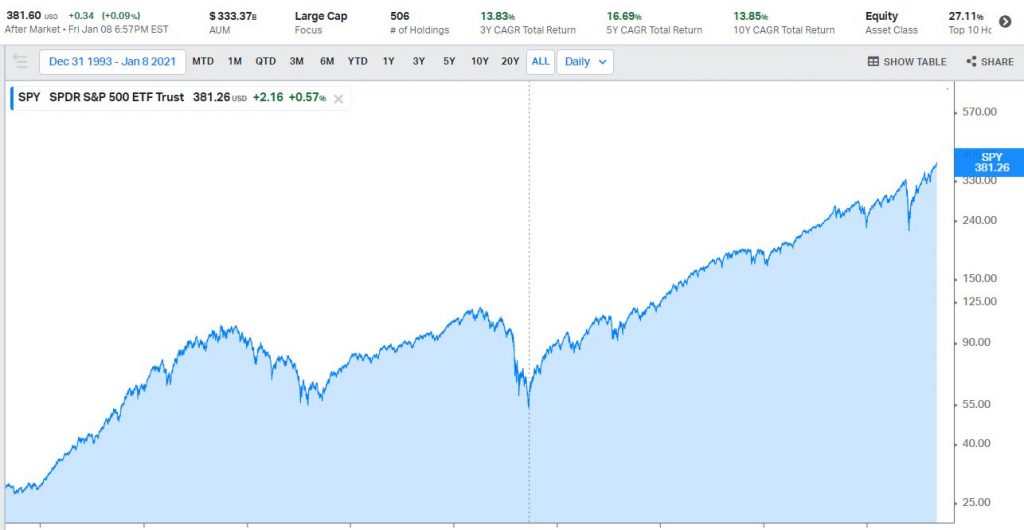

SPY – this ETF tracks S&P 500 an index that contains top 500 companies in the US. This is the index that is usually used as the benchmark for all returns. It is usually the case that if you can’t outperform this, you are better of putting all your money in it. As you can see, over the last 10 years, it has a cumulative average growth rate of 13.85%*. A massive one if you ask me. You will also notice it beats my 10% base rate. Check it out here – SPY for more detailed information.

Koyfin Charts by David Alade

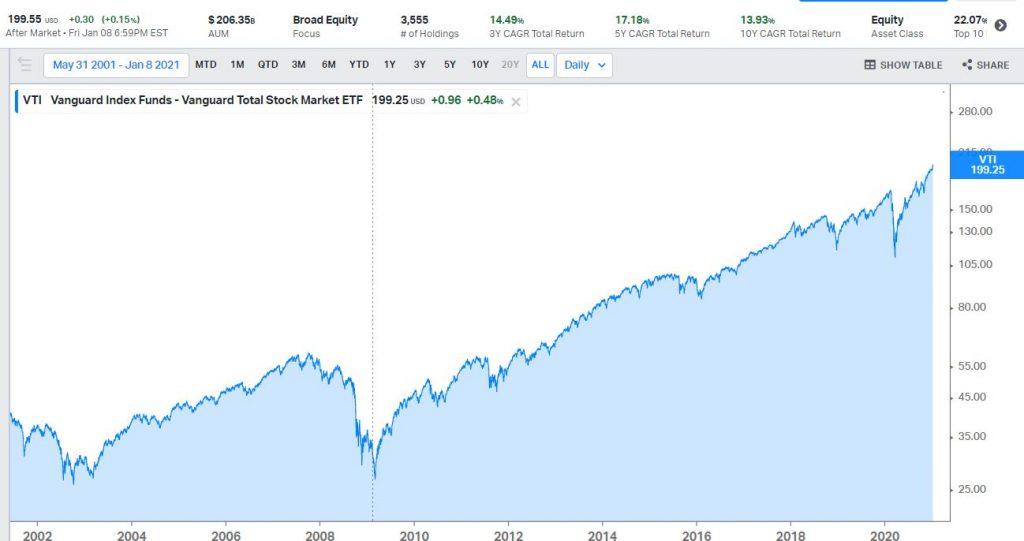

VTI – is an ETF that invests in all the actively trading stock in the US. It’s a total market cap fund. All good and all bad companies are in it. However, because the goods tend to do better enough to cover for the bad, it also has a cumulative average growth rate of 13.93%* in the past 10 years. Anyone invested in it is definitely better off. Probably what you should note is that these returns are despite the quite obvious massive deep of 2008. More on VTI here.

Koyfin Charts by David Alade

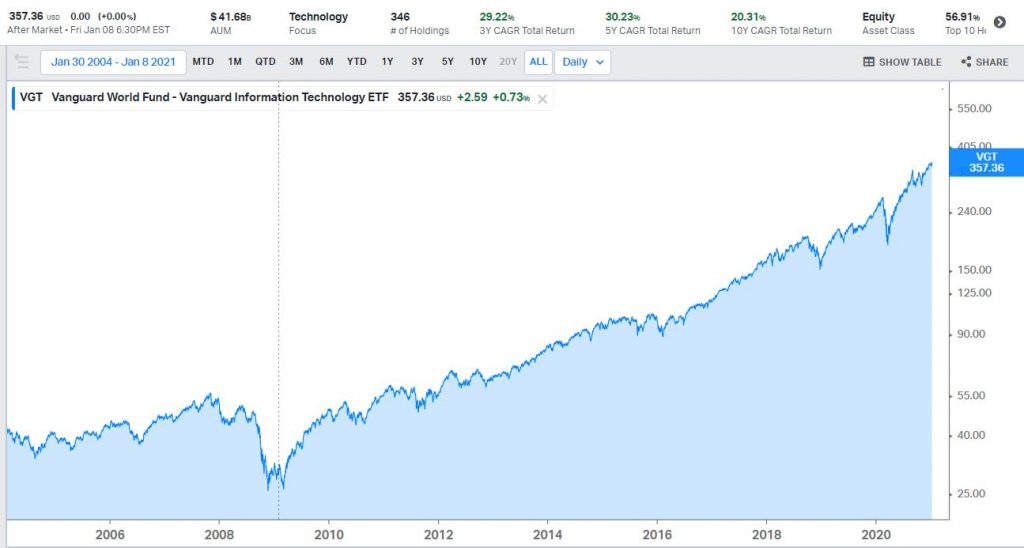

VGT – tracks the top 100 technology companies listed in the US. Companies at the forefront of innovation. Its cumulative average growth rate over the last 10 years 20.31%. This is a matter of getting 20.31%* average return on your investment for doing practically no work. Why would anyone want to take on any additional risk if you can just do the simplest thing and make this much return? I guess it’s the urge in us to make quick money. More on VGT

QQQ – like VGT also invest in top 100 technology companies listed in the US. The only difference is who manages them. And as you can see, it has a similar cumulative average growth rate with VGT at 20.25%*. Click here for more.

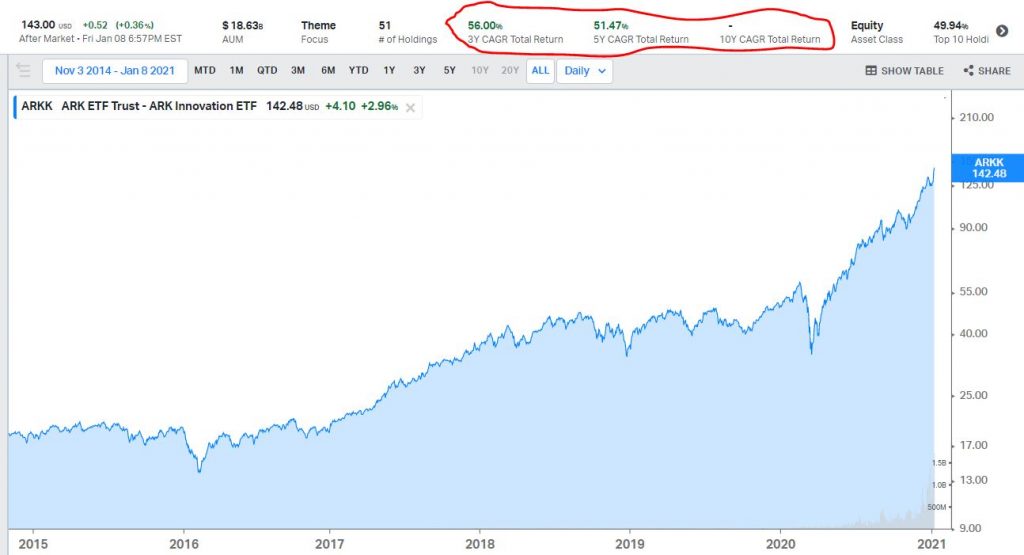

ARKK – ARKK is unique on this list as it is the only actively managed fund. Its goal is to invest in disruptive innovative companies. If you do not have 5-10 years investment horizon, you may not want to invest in this ETF. However, over the last 5 years, this ETF has a cumulative average growth rate of 51.47%*. That’s an impressive result at best.

Check out etf.com for more ETFs that are trading on the market. And if you are using Bamboo or Trove, you can easily see listed ETFs on the “featured themes” on the homepage from Bamboo and under the ETFs category from “All Assets” in Trove.

Please use the comment section to drop all your questions. I promise to answer them all.

Let’s build this wealth together and benefit from a generational opportunity.

Join 300+ people who are subscribed to my newsletter via this link to get notified of future posts like this and more.

Red Alert* – past performance does not in any way guarantee future performance. Also, this does not in any way constitute investment advice. All I’ve written so far are for educational purposes only.